A few charts to summarize the year 2023 in the markets. But first, a few headlines encapsulating the zeitgeist headed into last year:

Let’s not leave out the Journal:

Naturally, here’s how the major indices finished 2023:[i]

Here they are since the market bottom on October 12th of 2022:[ii]

The simple summary of the stock market in 2023 is a continuation of the rally that began mid-October 2022. Take a moment and try to remember mid-October 2022. Sentiment was awful. October 12th was the day the CPI (inflation) report for September was released – a scorching 8.2%.[iii] It was also four weeks before the mid-term elections. The red wave turned out to be a red trickle. Everyone was worried going into the midterms, and no one was happy afterwards. And yet… please reference again the above chart of stock market returns since one month before the ’22 midterms. People were worried about supply chains and the war in Ukraine (which was still dragging on by Oct. ’22, despite no one anticipating it lasting that long when it began in February). The Fed embarked on the fastest interest rate hiking cycle in its history in 2022 and continued in 2023. And yet... please reference again... Nevermind. I’m just going to post the same chart again to make sure you can’t avoid it:

2023 gave us another reminder of one handy rule of thumb: never take advice from famous investors who know nothing about you, your time horizon, risk tolerance, objectives, etc. Here’s Michael’s Burry’s (the hedge fund titan played by Christian Bale in The Big Short) now infamous tweet on January 31, 2023:

Maybe it was best not to follow Burry’s advice back in January? A few more thoughts on that here.

The lead story of 2023 in the markets was the outperformance of the “Magnificent Seven” stocks (Apple, Microsoft, Facebook (Meta), Google, Amazon, Nvidia, and Tesla). These seven behemoths drove the majority of the S&P 500’s return:[iv]

An interesting story, sure. Also one that conforms to two basic theories of mine:

- You can win (or lose) almost any argument about the stock market by changing start and end dates

- No one remembers what happened last year

Here is the Magnificent Seven and the S&P 500 from the beginning of 2022:[v]

So as magnificent as the returns of the Magnificent Seven have been, perhaps it was more a story of recovery after an abysmal 2022? From 2022 – 2023, the average return of six of the Magnificent Seven stocks is -2.19% compared to the S&P 500’s +3.42%. Nvidia is the outlier shown in pink above. The Magnificent Seven becomes the Magnificent One. Great, an outlier of a stock over a two-year period. That is not a story. It happens all the time.

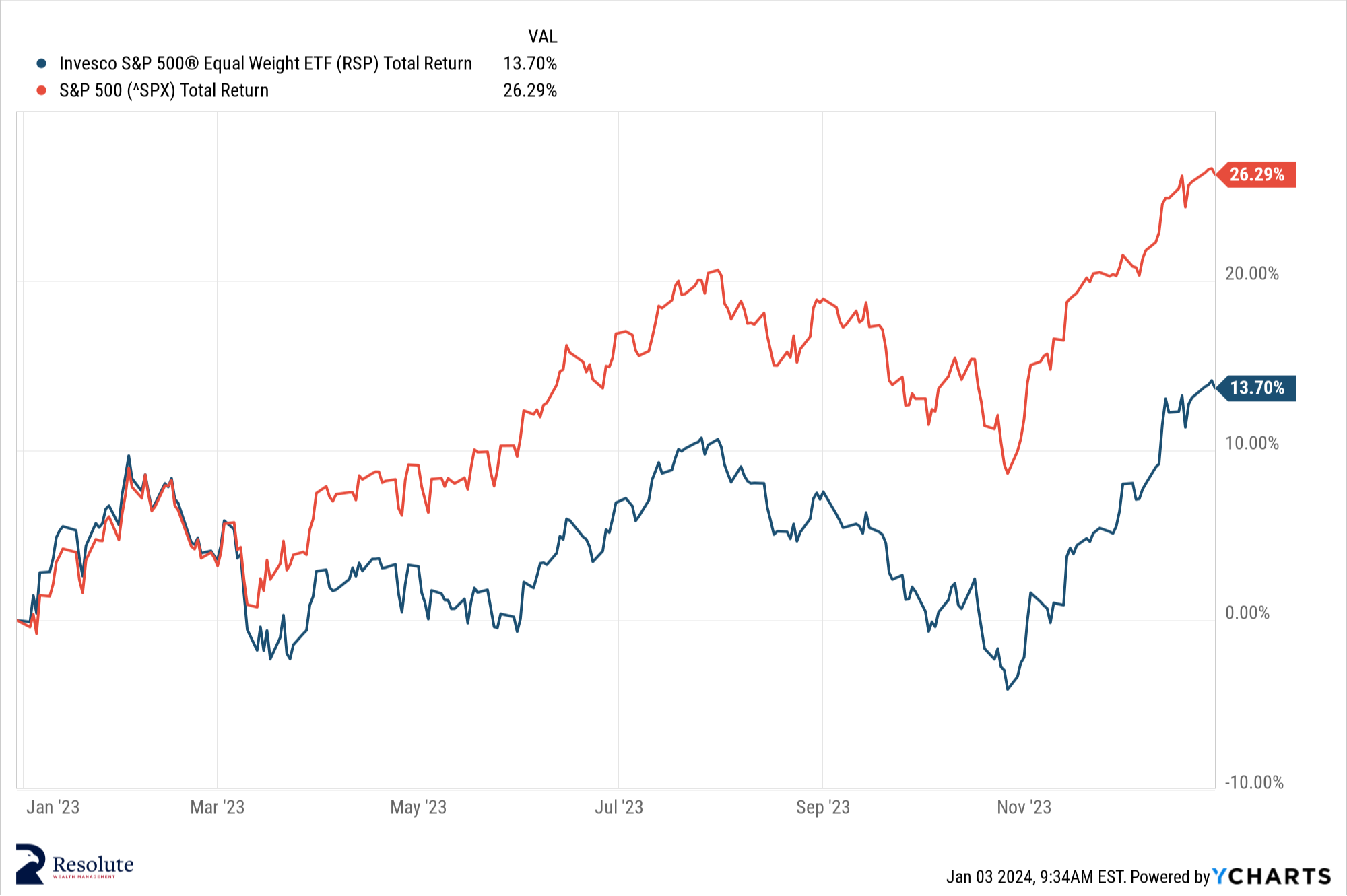

Much ink was spilled last year arguing the stock market’s returns being driven by a handful of stocks is a sign of weakness and reason to worry. Commentators pointed to the equal weight return of the S&P 500 vs the cap-weighted return. (Aside: the equal weight S&P 500 gives each of the 500 constituent stocks the same weight in the index, while the cap-weighted S&P 500 gives each of the 500 stocks a weighting proportionate to their market capitalization. When people talk about the S&P 500 or “the stock market” they are referring to the cap-weighted index). The Magnificent Seven are the seven largest holdings of the S&P 500, making up ~28% of the index. Here’s cap-weighted (red) vs. equal weighted (blue) returns in 2023:[vi]

And here’s cap-weighted returns vs equal weighted returns since the beginning of 2022:[vii]

A similar story to the Magnificent Seven – cap weighted underperformed in 2022 and caught up in 2023. Just change the start date and you paint an entirely different picture.

Remember the regional banking crisis? In March of 2023 two of the four largest bank failures in the history of the United States occurred within two days of each other. Silicon Valley Bank failed on March 10th followed by Signature Bank on March 12th. SVB was the second largest bank failure on record and Signature the fourth. First Republic Bank failed two months later, the 3rd largest bank failure in U.S. history.[viii] Three of the four largest bank failures ever happened last spring! No one seems to remember that. Silicon Valley Bank is another cautionary tale of the risks of trading individual stocks. Here are its returns since it’s 1987 IPO vs the S&P:

26,000% returns compared to 2,600% is nice. 10x the S&P! Then 2023 happens and SVB goes to zero in a few days.

Picking stocks is hard.

Gold hit an all-time high of $2,100/ounce in December of 2023.[ix] This is exciting for people who have been holding gold for a long time. Those who chose to invest their capital in income generating businesses don’t really care. Here’s $10,000 invested in gold vs. the S&P 500 since the first day of 1980 (gold investors, avert your eyes):

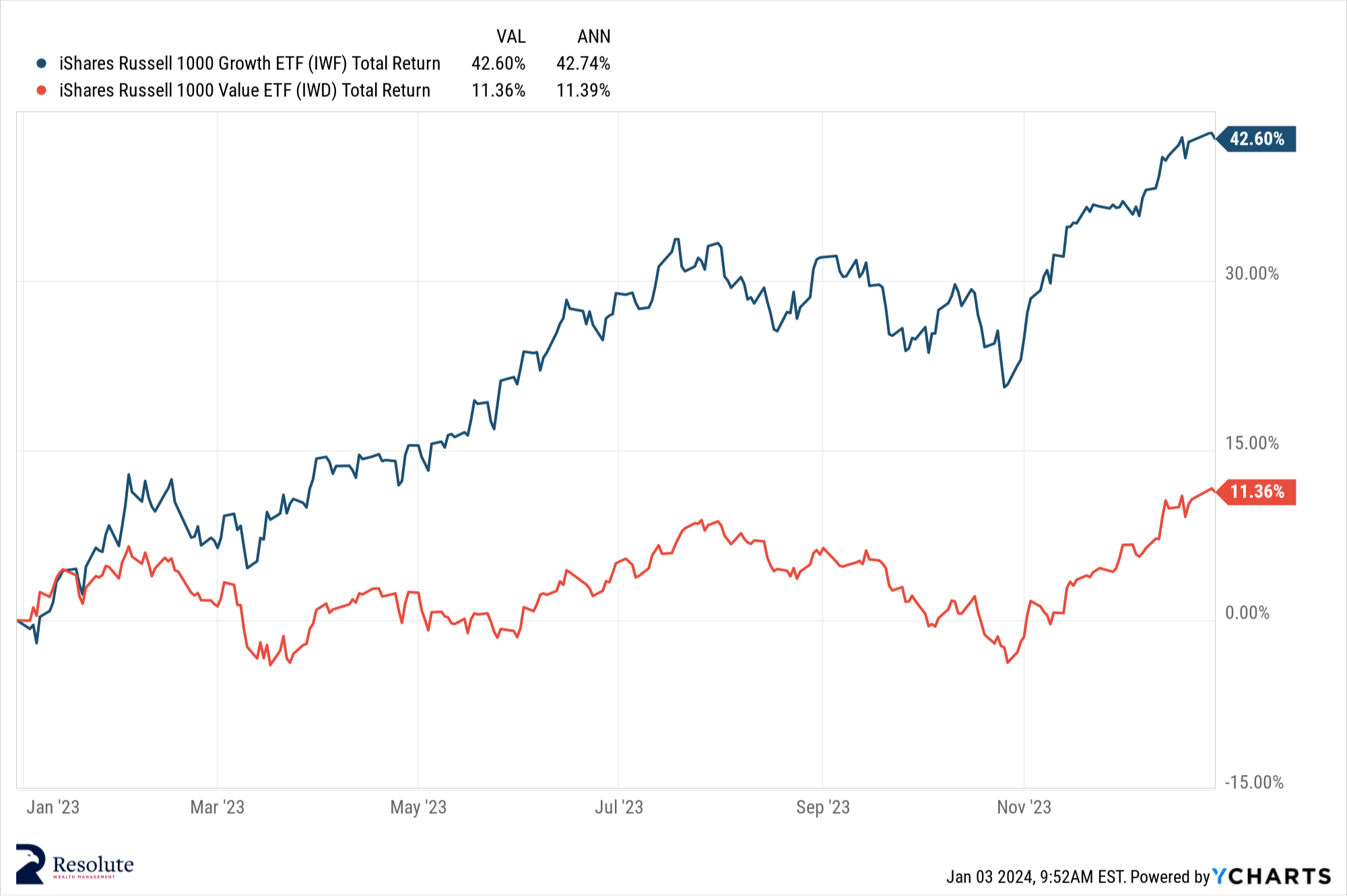

Growth outperformed value in the aggregate for 2023 – here’s the Russell 1000 growth (blue) vs Russell 1000 value (red) in 2023:[x]

Zoom out a bit and it’s much the same story as the Magnificent Seven stocks – move the start date back to the beginning of 2022 and 2023 just looks like mean reversion. In fact, value has a slight edge over growth the last two years:[xi]

Growth stopped lagging around the beginning of the year – an accident of the calendar. We don’t think anyone could have timed this shift without the benefit of hindsight, and we caution against trusting anyone claiming they can do so. We prefer owning both growth and value and rebalancing when appropriate.

Here’s inflation plotted alongside the federal funds rate (the rate everyone refers to when they say something about the Federal Reserve and interest rates) over the last two years:[xii]

Speaking of interest rates, here’s the 30-year mortgage rate over the last two years ending 2023 at 6.61% after a peak of 7.79% in October:[xiii]

Let's not forget the consensus trade going into 2023 was buying U.S. Treasurys. After an 18% drawdown in the stock market in 2022 and Treasurys suddenly yielding ~5%, you couldn’t listen/watch/read some media/opinion even tangentially tied to finance without hearing a recommendation to sleep well at night earning 5% “risk-free” in Treasurys. I am pretty sure people were talking about Treasurys at dinner parties in 2023. Treasurys! They even came up with a Gen-Z sounding name for the trade: “T-Bill and Chill.” Allocating money you plan to spend in a year or two to short-term Treasurys or money market funds is commendable. No sense exposing yourself to stock market volatility if you need the money soon. Unfortunately, many elected to T-Bill and Chill with dollars earmarked for long-term goals. Those folks got their faces ripped off:[xiv]

I noted many pundits pointing to some variation of the following chart as a harbinger of doom throughout the year. Here’s total US credit card debt going back to the turn of the century:[xv]

U.S. households hit a record $1 Trillion in credit card debt in 2023. A big, scary round number! But that number is meaningless without context:[xvi]

Credit card debt is at record highs, but household net worth is nearing record highs as well while debt service as a percentage of disposable income is in a secular downtrend. Context always matters. I wrote about this previously here.

Let’s move back a few years before 2023. Think for a moment everything that has occurred since the beginning of 2020. Pandemic, lockdowns, 2020 contested election, riots, war in Ukraine, worst inflation since the 70s, fastest interest rate hiking cycle ever, supply chain blockages, housing affordability crisis, mid-term elections, Hamas terror attack, to name a few. They say there are decades where nothing happens and years when decades happen. Lately it’s felt like the latter. Since 1926, the stock market has averaged 10% annually. Certainly it can’t have been anywhere near that 10% average since 2020…[xvii]

12.05% annualized return from 2020 – 2023. I bet you thought it was substantially lower.

2023 was a good reminder of perhaps the most astonishing fact about the stock market I have run across: the U.S. stock market has had more 20+% return years than negative years.[xviii] One more time, in case you glossed over that:

The U.S. stock market has had more 20+% return years than negative years.

Here is a great chart Ben Carlson put together:[xix]

The orange bars show each year’s S&P 500 annual return, while the blue line shows the annualized rolling 30-year return. Long-term investors would do well to internalize this chart and its glorious implications.

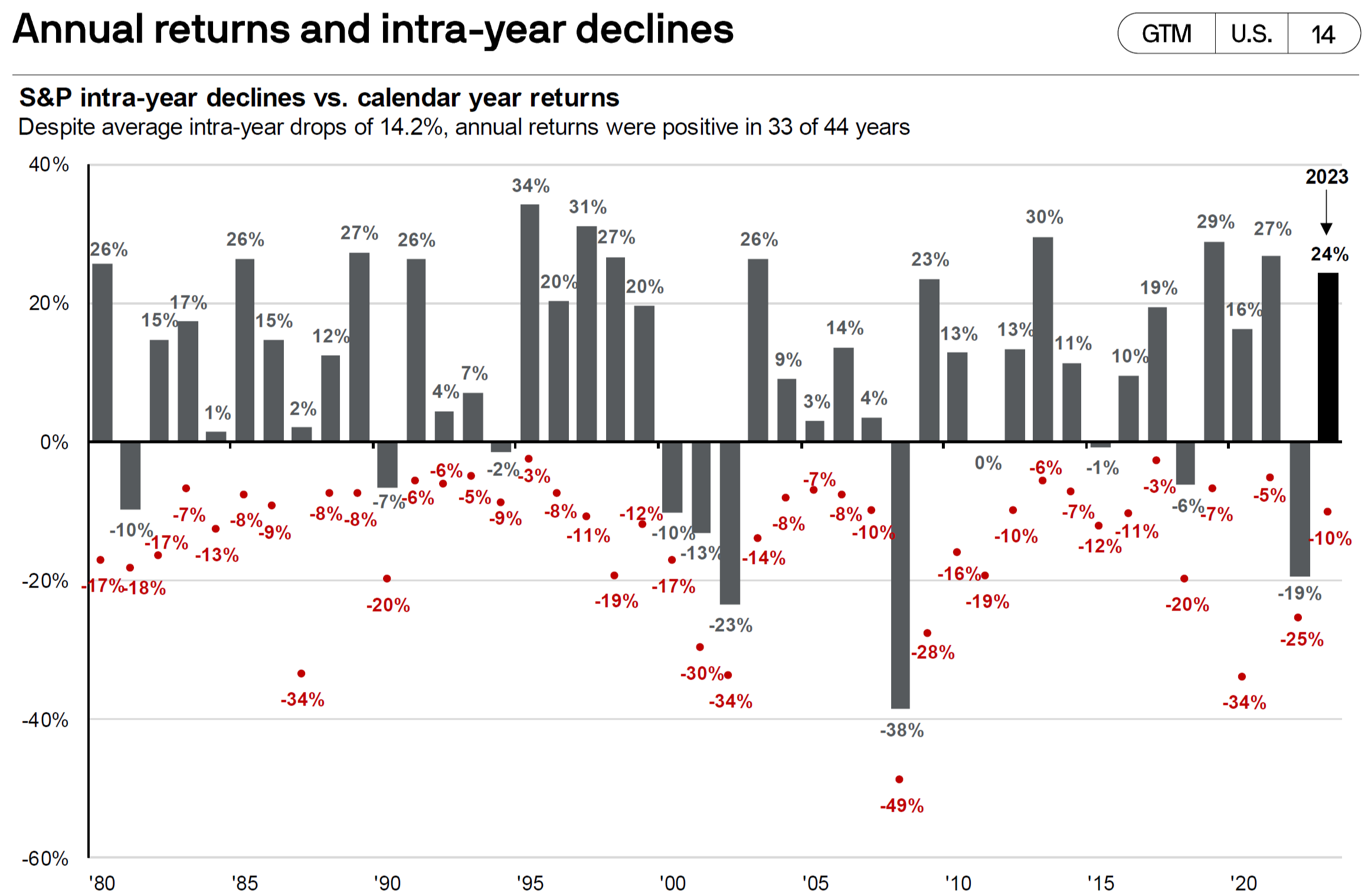

While 2023 was a great year in the market, it was not without volatility of its own. The S&P 500 saw a 9.81% decline from August through October, just 0.19% away from an official 10% correction. A 10% intra year decline in a year that returns 20+% ought to be expected (but never is). Here is my favorite chart (credit to JP Morgan for putting this together each quarter) showing annual returns plotted alongside intra-year declines since 1980:[xx]

Investors who were scared out of the market’s 9.81% three-month decline from August - October missed a 16.23% rally to year end that began on October 27th.[xxi]

I suspect the presidential election will be the worry du jour in 2024. Perhaps you are already worried about the impact of the election on your portfolio. Since 1928 (the Center for Research in Security Prices began putting together reliable stock market data in 1926), we have had 24 presidential election years.

The S&P 500 ended only four of those 24 years lower than it started.

Sean Cawley CFP®

Neither asset allocation nor diversification guarantee against investment loss. All investments and investment strategies involve risk, including loss of principal.

Content here is for illustrative and educational purposes only. It is not legal, tax, or individualized financial advice; nor is it a recommendation to buy, sell, or hold any specific security, or engage in any specific trading strategy. Results will vary. Past performance is no indication of future results or success. Market conditions change continuously.

This commentary reflects the personal opinions, viewpoints, and analyses of Resolute Wealth Management. It does not necessarily represent those of RFG Advisory, clients, or employees. This commentary should be regarded as a description of advisory services provided by Resolute Wealth Management or RFG Advisory, or performance returns of any client. The views reflected in the commentary are subject to change at any time without notice.

[i] YCharts, Fundamental Chart, Total Return Level, SPX/NDX/DJI/BBUSATR, 01/01/2023 – 12/31/2023.

[ii] YCharts, Fundamental Chart, Total Return Level, SPX/NDX/DJI/BBUSATR, 10/12/2022 – 12/31/2023.

[iii]https://cpiinflationcalculator.com/2022-cpi-and-inflation-rate-for-the-united-states/

[iv] YCharts, Fundamental Chart, Total Return Level, SPX/AAPL/MSFT/NVDA/GOOGL/META/AMZN/TSLA, 01/01/2023 – 12/31/2023.

[v] YCharts, Fundamental Chart, Total Return Level, SPX/AAPL/MSFT/NVDA/GOOGL/META/AMZN/TSLA, 01/01/2022 – 12/31/2023.

[vi] YCharts, Fundamental Chart, Total Return Level, SPX/RSP, 01/10/2023 – 12/31/2023.

[vii] YCharts, Fundamental Chart, Total Return Level, SPX/RSP, 01/10/2022 – 12/31/2023.

[viii]https://www.visualcapitalist.com/largest-bank-failures-modern-history/#google_vignette

[ix]https://www.cnbc.com/2023/12/04/gold-prices-set-for-new-highs-amid-economic-geopolitical-uncertainty.html

[x] YCharts, Fundamental Chart, Total Return Level, IWF/IWD, 01/01/2023 – 12/31/2023.

[xi] YCharts, Fundamental Chart, Total Return Level, IWF/IWD, 01/01/2022 – 12/31/2023.

[xii] YCharts, Fundamental Chart, Original, US Consumer Price Index YoY/Target Federal Funds Rate Upper Limit, 01/01/2022 – 12/31/2023.

[xiii] YCharts, Fundamental Chart, Original, 30 Year Mortgage Rate, 01/01/2022 – 12/31/2023.

[xiv] YCharts, Fundamental Chart, Total Return Level, SHY/SPX, 01/01/2023 – 12/31/2023.

[xv] YCharts, Fundamental Chart, Original, US Credit Card Debt, Max Timeline.

[xvi] YCharts, Fundamental Chart, Original, Us Total Net Worth/US Household Debt Service as Percentage of Disposable Income, Max Timeline.

[xvii] YCharts, Fundamental Chart, Total Return Level, SPX, 01/01/2020 – 12/31/2023.

[xviii]https://awealthofcommonsense.com/2023/12/what-happens-after-a-20-up-year-in-the-stock-market/

[xix]https://awealthofcommonsense.com/2023/07/one-year-returns-dont-matter/

[xx]https://am.jpmorgan.com/us/en/asset-management/adv/insights/market-insights/guide-to-the-markets/

[xxi] YCharts, Fundamental Chart, Total Return Level, 10/27/2023 – 12/31/2023.